Introduction

The first module of Business Management is split up into two main categories:

1. Marketing

2. Accounting and Finance

There are three sections in the Marketing Category.

10.1 Marketing Analysis – In this section you are expected to know all about how a market for a given product or service is formed, including looking at things like segmentation analysis, market size, market growth and market share. These are all explained in detail later.

10.2 Marketing Strategy – In this section you need to understand exactly how a market works and what strategies are employed by companies in order to maximise profits. This includes things such as the Marketing Mix the Product Life Cycle theory and the Boston Matrix.

10.3 Marketing Planning – In this section you are expected to understand the need for companies to plan where and how their product will be placed and for what reasons. This includes things such as the pros and cons of different pricing methods and the applications of price elasticity of demand.

· There are four sections in the Accounting and Finance category.

10.4 Analysis of Finance – In this section you need to know about costs, profit contribution and breakeven analysis and be able to apply their formulas when answering number based questions. This includes knowing all the terms for costs and income.

10.5 Company Accounts – In this section you’ll learn about cash flow forecasting, the differences between cash flow and profits and the importance of both and ways of controlling and or improving cash flow for a business. This includes things like factoring and sale and leaseback.

10.6 Budgeting – In this section you need to know all about the advantages and disadvantages of budgeting, coupled with role of budgeting in management accounting. This includes stuff like calculating variance, and the uses of zero budgeting.

10.7 Cost and Profit Centres – In this section you learn about the purposes of cost centres and profit centres and how they can help to organise and motivate businesses and help them to develop into effective and profitable firms.

As you can see the fun never stops in the world of business! J

Marketing

Analysis

Although revision is the devil it’s best to get stuck in so let’s begin with Marketing Analysis. Woo Hoo!

So what is marketing? This is the definition that you need to know to get the marks in the exam.

· Marketing is a management process aimed at identifying, analysing and satisfying customer requirements usually at a profit.

This is definitely something that needs to be learnt off by heart as it is a fairly specific and thorough explanation of what marketing is. The effectiveness of marketing however depends on exactly how much a firm knows about its market. This includes the size of the market, the potential for the product or products the firm is marketing to grow, and the market share that a particular firm has.

Markets are usually split up into loads of different segments. As a result a business needs to ensure that they know exactly what their target market is including all of the possible market segments to which it will apply. Knowing your market is a fundamental part of market analysis and an incredibly important task for any developing business.

An example of how a market can be split up into different segments is as follows.

Market

segmentation for the fashion industry:

Clothes Accessories Famous Designers

Jeans, Dresses, Shirts Belts, Handbags, Shoes Calvin Klein, Dior, Versace

As you can see this is a very simple example of how an incredibly large market could be split up. There are hundreds of other segments which could be branched off each of the above subheadings so you can imagine how important it is for a company to ensure their product has an established and well defined target market.

The only way to give a product the best chance of succeeding

is by undertaking market analysis.

This can be done by: Statistical Analysis, Market

Research or SWOT Analysis

SWOT Analysis is an important market analysis tool. SWOT stands for:

Strengths Weaknesses Opportunities and Threats

|

SW |

Analysing the strengths and weaknesses of a

business is known as an Internal Review. An internal review focuses on

what the business is doing well and refers to everything that a company has

already achieved or is in the process of achieving. It also highlights areas

in which the company needs to improve in order to be able to compete in the

market. This includes things like Company Reputation and Market

Representation. |

|

OT |

Analysing the opportunities and threats to a

business is known as an External Review. An external review focuses

more on factors affecting a business that cannot be controlled by the firm

itself. This includes things such as the State of the Economy,

advances in Technology and progress of competitors. |

Market Research is also a very important factor when analysing a market. Market research can be split up into two categories, Primary and Secondary. Here are a couple of definitions for these two terms that also could do with being learnt:

Primary Market Research - Research carried out by or on behalf of a firm which is specific to that firms needs, also known as field research.

Secondary Market Research - Research used by a firm or company which has already been carried out by some other source. Includes things such as government statistics.

Statistical Analysis, another useful market analysis tool is somewhat linked to primary and secondary market research. It involves the collection and or interpretation of statistics either from a primary or secondary source. Statistics can also be categorised as Quantitative or Qualitative data.

Ways in which these statistics can be collected are as follows:

- Sampling- Random Sampling or Quota Sampling. This is a method of splitting up a population in order to save time and money when surveying them.

- Creating a questionnaire. Questionnaires are cheap and easy to produce however they have drawbacks such as low response rates and unreliable data.

- Conducting a series of face to face interviews. Interviews generally create more reliable data but they are time consuming and hard to do a lot of them, this could make the data biased.

Once a company has conducted their research and gained all the relevant statistics their preliminary market analysis is complete. This research can then be given a Confidence level which is a measurement of how accurate and reliable they think their research is.

Key

Terms

Market Segment - A group of customers with similar characteristics to each other, for example the over 60’s. It can also be defined as a subsection of a section of a larger market.

Market Size - The size of a market in terms of volume of sales or value of sales. (Assuming value is price x quantity)

Market Growth - The percentage rate at which the size of a market is increasing.

Market Share - The percentage of a particular market accounted for by sales of a particular firm. The firm with the most sales has the largest market share and is subsequently known as the market leader.

Primary Research - Research carried out by or on behalf of a firm which is specific to that firm’s needs. Also referred to as field research.

Secondary Research - Research used by a firm or company which has already been carried out by some other source. Includes government statistics.

Sample - A subset of a market chosen for research purposes because it is too expensive or unrealistic to interview every member of the target market. The bigger the sample the more likely it is that it will be representative of the market.

Random Sample - A sample in which every member of the population has an equal chance of being selected.

Stratified Sample - A sample which is chosen so that it reflects the composition of the market being researched. I.e. if one third of customers are female then one third of the sample will be female.

Quota Sample - A means of getting a stratified sample. Researchers are told to interview a particular quota of certain types of people so that the final sample reflects the composition of the market.

Quantitative Research - Research which involves the use of numbers in its results for example number of people who buy a product.

Qualitative Research - Research which does not involve numbers, instead involving a response which reveals what people think of a product.

Confidence Level - A measure of how reliable a

firm thinks its’ research is. For example a 95% confidence level means the firm

believes that the research is likely to be accurate 95 times out of a hundred.

Marketing

Strategy

If a question comes up in the exam about marketing strategy

then straight away you should be thinking about exactly what this means in

English. Basically what does a company have to do in order to make sure their

product has a positive impact on their market?

When coming up with a marketing strategy it is important for a company to know exactly what it wants to achieve. For this to happen a company needs to have objectives, once it has done this a strategy can be worked out around these objectives. A marketing strategy therefore is the steps you take in order to meet your objectives.

Once a company has set up their objectives there are many

ways in which it can develop its marketing strategy. One of these ways is

through Product Differentiation.

Product Differentiation is an extremely important part of successfully marketing a product. As a result it will almost certainly play a significant role in successful marketing strategy.

The Definition of Product Differentiation: adapting a product in order to make it stand out, perhaps by giving it unique features or by branding it.

When thinking about implementing a marketing strategy a business needs to take into consideration how they are going to meet the needs of their user as well as their own objectives. As a result some areas of the marketing mix will need to be stressed above others in order to focus on particular benefits. For example if a company were looking to increase their market share they would need to focus on price and introduce a penetrative pricing scheme meaning low margin of profit on each sale but increasing market share for the product. Another example would be if a product were aimed at a particular target group for example women - then promotion would need to be focused on in order to ensure the advertising was effective at bringing in customers from the target demographic.

There were a few terms in that paragraph that probably need further explanation.

Marketing Mix - The elements necessary to successfully

market a product, commonly known as ‘The Four P’s’ – Price, Place Product,

Promotion. (However there are more, so don’t limit yourselves to these four and

don’t forget about Planning.)

Once you’ve talked about how a company is going to deal with

their product - hopefully talking about product differentiation and the

marketing mix - then you need to start thinking about what kind of market the

product would be aimed at. This is where you need to bring in knowledge about mass

marketing and niche marketing.

We’ll start with definitions:

Mass Marketing- Devising a product with mass appeal and

promoting it to everyone.

Niche Marketing - Tailoring a product to a particular

segment of a larger market

Mass marketing

is useful for the plain and simple reason that it appeals to a lot of people.

This means that although your product is likely to be unoriginal, it will

always have a solid base of customers because of its mass appeal. This includes

products like crisps, chocolate, DVD’s etc.

Niche marketing on the other hand is very different. Niche Marketing focuses on a market segment or a subsection of a larger market and tailors a product to meet the needs of that segment. This can be more risky, your target market becomes smaller and far more concentrated however this enables a firm to get closer to their market and this could result in more sales due to a better knowledge of the firms’ customers and what they want from a certain product.

Here is a breakdown of the advantages and disadvantages created by Mass and Niche Marketing,

Mass Marketing

Advantages:

- Mass marketing is all about low cost production with an emphasis on large scale manufacture of goods. This provides opportunities for companies to benefit from economies of scale such as bulk buying etc.

- Production of a variety of different products sold in various different markets reduces the risks of an economic recession or fall in demand for a certain product.

- Mass production will greatly improve short term cash flow as manufacturing output is at extremely high levels, combating problems companies may face with working capital. (For example if a company were to withhold payment for a purchase of stock from your own company, it would be less damaging if your company is constantly making lots of sales.)

- Mass marketing can be beneficial to a product which is standardised and has a long life span. (See Product Life Cycle)

Disadvantages:

- Profit

margins for a product which is mass produced and mass marketed will be lower

in relation to differentiated products in a Niche marketplace. (Due to

lack of Unique Selling Point.) This in turn increases the Break Even point

for a product which is mass marketed.

- Companies who employ a mass marketing scheme are more likely to encounter diseconomies of scale including things such as lack of morale amongst staff.

- Mass marketing and large scale production may also create the problem of large, ineffective management structures which make communication between staff difficult and can hinder production due to its inability to respond to changing trends in the market.

Niche Marketing

Advantages:

- If a firm was able to identify a viable and relatively untouched market segment where demand is growing, then the chances for that firm to become profitable in the short term are extremely high.

- The financial risks of niche marketing are balanced by the fact that investment need not be high and only small amounts of funding are required.

- A

company which employs a niche marketing strategy is likely to have an

effective management structure due to lower levels of staff and therefore

lower levels of corporate bureaucracy,

making decision making process much more streamlined and time-effective.

- Staff feel far more valued as

they become specialists in a less competitive environment. Staff morale

levels increase hence increasing productivity levels for the company.

- Companies operating in a Niche

Market do not suffer from the same diseconomies of scale that larger

companies must handle.

Disadvantages:

- The expansion and growth of the firm depends solely on the expansion and growth of the market. If a company cannot encourage a significant consumer interest in their product range then the long term profitability of the company is compromised.

- Small scale Niche operations are not able to benefit from the advantages of economies of scale which larger firms can enjoy.

- Niche markets are sometimes unstable and occasionally suffer from the ‘straw on fire’ effect which refers to the market merely being a temporary solution to what is essentially only a fad. This is extremely detrimental to a company’s profitability.

- Unless a firm operating in a Niche market can establish a strong and sustainable USP then the firm will face challenges from larger companies who diversify into the niche market with one of their product ranges. Control of a particular market segment will also be lost if the factor affecting demand is price, due to the fact that mass produced products are invariably cheaper.

Although this is mind-numbingly boring its worth getting learnt as it will most definitely be applicable to some aspect of your exam!

You’ll be happy to learn that the next few pages involve much less writing to give your eyes a well deserved break.

The Product Life Cycle

This diagram is an example of what is known as the Product Life Cycle. The Product Life Cycle is a predictive theoretical model of how a successful business or product should behave in terms of sales and cash flow throughout the product or business’s lifespan.

In terms of the product life cycle’s usefulness as a strategic marketing tool, it most definitely has its limits and is considered to be only really useful in hindsight, for analysis of a particular business’s performance.

Product Portfolio Analysis

Product Portfolio Analysis is a marketing strategy which aims to create a variety of balanced products which have a widespread appeal and hence will be supposedly profitable. This theory is best shown by the Boston Matrix:

HIGH Market

Share LOW

|

Rising

Star This is a product which has a high percentage market

share in a quickly growing market. |

Problem

Child A product which has low market share of a quickly

growing market. (High Potential Growth.) |

|

Cash Cow This is a product which has high percentage market

share in a slow growth market.

|

Dying

Dog A product which has low market share in a slow

growth market. (Low Potential Growth) |

HIGH

Market

Growth

LOW

The most important thing to realise about these two marketing strategies is that they are both useful for adding value to a company. The Product Life Cycle does this by making companies aware of the finite nature of their product. Once a company realises this they are much better equipped to continue the success of a product by avoiding ‘Determinism’ (see key terms) and hence improving their products’ lifecycle and profitability by coming up with some sort of extension strategy for that product.

The Boston Matrix

is useful as it allows managers to plan any further strategies they may need,

by organising their existing products into the categories set out in the

Matrix. For example a certain company may have too many ‘Dying’ dogs and as a result invest in Research and Development in order to develop a new range of

products to replace these dogs hence saving the company huge amounts of money,

and improving the company’s image.

Marketing Planning

Now my fellow business buddies we arrive at the Marketing Planning chapter, I hope you know what’s next……. yes that’s right it’s the Marketing Mix……………..

As was mentioned previously the marketing mix is defined as: The elements necessary to successfully market a product, commonly known as ‘The Four P’s’ – Price, Place Product, Promotion. This is important guys, so listen up.

Price

Factors influencing price are based on supply and demand. Demand is affected by quality of product, consumer incomes, competitors, tastes and fashion. Supply is affected by costs of input (wages and raw materials), technology, and production methods. The competitiveness of the market is perhaps the most influential factor for a company deciding on a method or methods of pricing and the firm’s power to set market leading prices will depend exclusively on that firm’s market share.

A few examples of different pricing methods are:

Cost-Plus Pricing: Price is average cost plus a percentage ‘mark up’ for profit.

Price Discrimination: Price is raised or lowered for different people wanting the same thing.

Contribution

Pricing: Price is set to cover variable costs and contribute to fixed

costs until break even is reached whereby fixed cost contribution becomes

profit

Examples of pricing strategies are:

Skimming: High price to begin with, yields big profit margins, followed by a drop in price when competitors enter the market in order to establish market share.

Penetration: Low prices set in order to increase market share.

Price Leaders: A company with high market share sets a price that smaller firms are forced to follow.

There are a few more of these strategies and methods but I’m a revision guide not a teacher so you should already know the others!

Place

Place refers to exactly where your product is going to be in order to achieve maximum consumer exposure. The Placing of your product can be vital to its overall success and needs to be somewhere where your target buyer will see it frequently. For example it’s no use trying to sell the latest most expensive Rolex in Oxfam because the people looking to buy the most expensive Rolex won’t be looking in Oxfam for it.

The Traditional method of getting a product from producer to buyer was:

Producer

Wholesaler

Retailer

Consumer

However many companies now bypass the wholesaler for cash flow reasons and some companies such as Dell, go straight from producer to consumer via the internet, a unique and interesting way of developing their own USP.

Product

If you don’t have a viable, sellable product then all of the other P’s become redundant and unnecessary. You must have a product which has a USP and is differentiated from the rest of the market in order for all of the other aspects of the marketing mix to fall into place.

Promotion

Once a product has been established, Promotion aims to persuade all of your potential customers to part with their cash, whilst also attempting to draw the consumer’s attention to your brand above anyone else’s. This can be done in two ways:

Above the line Promotion- Advertising through the mediums of the mass media including T.V, Newspaper and Radio adverts.

Below the line promotion- Also referred to as ‘in house’ promotion it includes methods of promotion such as merchandising, canvassing, personal selling and direct marketing.

O.K That’s the worst of it done with, just remember that the four P’s are not equally important in all situations and different circumstances call for different aspects of the mix to be given more attention than others.

To summarise this section, the integrated nature of any marketing decision calls for the use of a variety of different marketing strategies to be implemented in order to create the strongest possible position in the market for a particular company. REMEMBER IT !!!!!!!!!!!

As you already know, ‘Price’ is one of the most important elements of the marketing mix and it is also an integral part of another section of the syllabus:

Elasticity of

Demand

One of the most important concepts of any firms pricing strategy is the relationship between supply and demand. A company needs to know exactly how the market will respond to a change in a certain product’s price, so that they can make the most out of constantly changing economic conditions.

There are two main types of elasticity that you need to be aware of for the exam, the first is Price Elasticity of Demand or PED, very important, the second is Income Elasticity of Demand, IED, also important but we’ll come back to that later.

So what is Price Elasticity of Demand?

PED is defined as the responsiveness of demand to a change in price. But what does it mean?

It means that it is a measurement of how much demand will go up or down if a product were to increase or decrease in price.

The way to remember this is by this incredibly important formula:

PED = %change in

Demand

% change in Price

If you’re not mathematically minded don’t worry, all you have to do is substitute numbers into this formula, it’s just a matter of learning all the types of questions you might be asked concerning this formula.

Remember these facts and you should be fine.

Price Elastic means that a lower price will result in an increase in revenue for a particular product. This is expressed in the formula by a PED of 1 or over. (If answer is negative ignore minus sign)

Price Inelastic means that a price rise will lead to a revenue rise. This is expressed in the formula by a PED which is less than 1. (Usually a decimal. Ignore minus sign if negative)

Here is a good way to remember it:

|

Price |

Demand |

Revenue |

|

£10 |

100 |

£1000 |

|

£11 |

98 |

£1078 |

With this product a rise in

price has lead to a rise in revenue. The product is therefore Price Inelastic.

|

Price |

Demand |

Revenue |

|

£10 |

100 |

£1000 |

|

£11 |

90 |

£990 |

With this product the revenue

was more when the product was at its lower price- Price Elastic.

Here’s an example question and answer to start you off with.

1. Success to A* Ltd plans to increase its prices by 15% Given that the marketing division believe hat their product has a price elasticity of 0.5, calculate the company’s revenue following the price rise. The starting price for their guide is £3.00 with a starting demand of 1,500,000 customers.

Answer: PED = %change

in Demand

% change in Price

Step 1: Always write the formula out as you get marks straight away just for this.

PED = %change in Demand = 0.5

15

Step 2: Next step is to sub all the numbers in that you know from the question, as I have here.

Therefore: X = 0.5

Step 3: This is the maths bit! As the % change in demand is unknown we replace it with an ‘X’. From here we rearrange the equation to find the value of ‘X’.

‘X’ = 0.5 x 15

‘X’ = 7.5

PED 7.5 = 0.5

15

Step 4: By substituting the value we found for ‘X ‘back into the original formula we can check that the value we have calculated is correct, in this case it is.

Price Increase is:

£3.00 x 1.15 =

£3.45

Step 5: Now we can calculate the new price of the guide; (an increase of 15 %) and the new demand for the product; (an increase of 7.5%).

Demand increase is:

1,500,000 x 1.075 = 1,612,500

Revenue = Price x quantity

Step 6: By using the formula for working out revenue, (R = P x Q), we can substitute in our values from the previous step and calculate our final answer!

Revenue = £3.45 x 1,612,500

Revenue = £5,563,125

I can promise you that this is one of the hardest types of question on PED you are likely to get, most questions will simply ask you to work out the PED of a product by giving you some variables so basically Steps 1-4. However be prepared to answer questions like this one!

Now we move onto Income Elasticity of Demand- pretty similar to PED but with a few distinct differences.

Income Elasticity is defined as the responsiveness of demand to changes in income.

The formula for this is pretty similar to PED.

IED = % change in Demand

% change in Income

The ‘Income’ part of Income Elasticity is referring to the

Income of the population i.e. the average income of

If a company is able to calculate IED then they will be able to predict exactly how much a change in income will affect demand for their products.

When thinking about IED you need to remember that goods, services and products sometimes be classed as superior or inferior.

- Superior goods are goods which- when consumer income falls- demand for these products fall. They are also known as

luxuries and are generally products which consumers feel are not necessary and do not buy

because they have less dispensable

income. A good example is a top of the range Jacuzzi bath or an

expensive

- Inferior goods are goods which- when consumer income rises- demand for these products fall. The demand falls for these products because consumers can afford to buy higher quality alternatives because they have more dispensable income. An example of an inferior product would be all ‘Economy’ ranges at Tesco or ‘Smart Price’ Ranges at Asda.

So Remember:

Income Inelastic products are products where demand for it is not affected by changes in income and these products are generally necessities such as petrol or addictive products such as alcohol and cigarettes.

Income Elastic

products are products where demand is affected by changes in income and this is

true of most products especially

Accounting and Finance Analysis of

Finance

We have now arrived in the wonderful world of Accounting and Finance! This section is generally a lot less wordy but relies on you learning formulas and methods of working things out as well.

Costs

As with any Business their will always be costs. What you need to know for the exam is that costs can be split up into a variety of different categories.

Fixed Costs- Fixed costs are defined as costs which do not change in relation to output. For example: Salaries or gas bills.

Variable Costs- Variable costs are defined as costs which do vary with output. For example: raw materials or packaging.

Direct Costs- Direct costs are costs which can be directly attributed to the production of a particular product and allocated to a particular cost centre. I.E Piece rate pay.

Indirect Costs- Indirect costs cannot be as closely allocated in this way. Indirect costs may also be known as overheads. I.E. marketing

There are a few formula’s which you need to know for cost, they are simple but their also very important so they should be learnt.

Total Cost = Fixed Cost + Variable Cost

(TC) = (FC) + (VC)

Average Cost = Total Cost

(AC) Output

Another aspect which businesses have to control is Revenue and Profit which are two completely different things. These formulas should help to stop you from getting them confused.

Revenue = Price x Quantity (of sales)

(R) = (P) x (Q)

This is the formula for Revenue.

Profit = Revenue – Total Cost

(P) = (R) - (TC)

This is the formula for Profit.

Break Even Analysis: Break-Even Charts

Break even analysis is perhaps one of the most important aspects of the Accounts and Finance section of Module 1. Let’s start with a definition of break even.

Break Even- Break even is the point at which a company’s Revenue is equal to their Total costs and as a result the point at which the company is making neither a loss nor a profit.

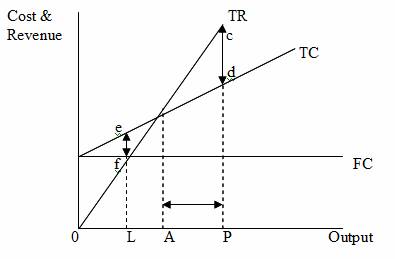

In your exam you could be asked to draw what’s called a Break Even Chart which looks a bit like this:

This at the moment probably means nothing to you but this description should help to clear things up:

- The Break- even output is at ‘A’ (See calculating Break even output)

- The distance ‘AP’ represents the margin of safety if the firm is producing at ‘P’

- The distance ‘cd’ represents the profit made if output is at ‘P’

- The distance ‘ef’ represents the loss made if production is at ‘L’

- FC is Fixed Costs

- TC is Total Costs

- TR is Total Revenue

Calculating Break-Even Output

To begin with it’s probably worth defining exactly what Break Even Output is. Break even output is the level of production (output) that a company needs to reach for revenue to equal costs.

In the exam you may be asked a question which involves you calculating Break Even output. So it’s a good idea to learn these next few formulas.

Calculating BEO revolves around the concept of contribution. Contribution is basically

The amount of money left over once variable costs have been covered.

For Break Even Output we need to know a slightly more specific form of contribution which is called Contribution per unit. This is worked out as follows:

Contribution per unit = Price – Average Cost

(Revenue per unit) – (Cost per unit)

Note: Average cost is sometimes called variable cost per unit as well.

This contribution is then used to pay off all fixed costs and once this has been done contribution goes towards profit.

Now your ready for the Break even output formula- brace yourselves it’s a bad boy.

Break Even Output = Fixed Costs

Contribution per unit

Here’s a quick example. Price = £17 Average Cost = £9 Fixed Cost =£1456

Break Even Output = 1456 = 1456 = 182

Units

17-9 8

This means that for this particular product to break even 182 will have to be sold.

Company Accounts

This section is all about Cash Flow Management. As always I’ll start with a definition.

Cash Flow- Cash Flow is the money flowing into and out of a business.

Net Cash Flow- Net Cash Flow is the difference between the money which comes in and the money which goes out.

Cash flow management is about the short term control of cash in order to ensure all short term debts are managed. Cash flow is incredibly important because if it is not managed properly firms which are essentially profitable can still fail if the firm is unable to pay a creditor who requires payment quickly and in cash.

In order to manage Cash Flow effectively, firms can take a number of steps. One of these steps is to invest time into drawing up Cash flow forecasts. This enables an organisation to identify potential problems and take appropriate financial action. For example: arranging a bank overdraft.

Why bother with Cash flow forecasting?

Cash flow forecasting helps business’s to:

- Forecast periods in a business’s or product’s lifecycle where cash outflow may exceed cash coming in.

- Plan how to finance major areas of expenditure.

- Ensure that liquid assets are available to meet debt payments.

- Highlight periods where cash is in excess and can therefore be profitably invested in some other aspect of the business.

- Justify to lenders/creditors that any money owed can and will be paid.

How can Cash flow be improved?

There are many ways of managing cash flow in order to improve a firm’s financial position.

Some are short term solutions whereas others may be more suitable as long term arrangements.

Stock Management: Managing stock is crucial in determining the strength of a company’s cash flow position especially regarding businesses that rely heavily on the rotation of stock from warehouse to shop floor i.e. supermarkets. If a company were to have high stock levels they would benefit from the advantages of bulk buying and other economies of scale. However they would suffer with the problem of storing all the stock and run the risk of losing money on stock which spoils easily or have low sell by dates.

Sale and leaseback: This involves the sale of assets in order to boost cash flow in the short term. Once assets have been sold i.e. property they may need to be leased back in order to continue the business function. This may be necessary for companies in need of a lump sum.

Debt Collecting: Although this may seem obvious, the collection of debts from firm’s owing you money is extremely important in maintaining a strong cash flow position. If a firm decides to delay payment of their debt then an option is to bring in a factoring company. Factoring companies operate by giving the company owed money an immediate lump sum of cash whilst collecting the debts owed to that company for themselves, whilst obviously charging for the service. Debt collection becomes even more important when looking at the way in which most businesses operate on a B2B (Business to Business) basis. What this means is that the likelihood of debts being withheld increases due to the fact that each company involved has to look out for their own cash flow position and will delay payment often in order to improve their own cash flow.

Sources of finance

As well as Cash Flow and Profit there is also another term referring to another use of cash within a business and this is finance. Finance is a term used to describe money which is solely used to cover company expenditures, of which there are two different types:

Revenue Expenditure: This is expenditure which takes place on a day to day basis and covers costs such as wages and raw materials. This type of expenditure generally provides a quick return due to the productive nature of a workforce and the fact that raw materials are going towards the production of products available to sell. Companies therefore need only rely on short term sources of finance for this type of expenditure.

Capital Expenditure: This expenditure revolves around the purchase of fixed assets which can be used numerously for the benefit of the company. For example: a new machine in a factory. It is probable that these items will be expensive and take a long time to cover the cost of their purchase so as a result long term sources of finance are required to cover this sort of expenditure.

In terms of different sources of finance there are many but they can be categorised into these two main categories:

External Sources: This refers to sources of finance which are unrelated to the cash generated by the internal sales from a particular company and include things such as Venture Capital, Bank loans, Bank Overdrafts, Debentures and shares, all of which you should have learnt in your lessons.

Internal Sources: As the name suggests these sources

of finance are produced internally

and are directly related to the cash

generated by a business in terms of how often they can be relied upon. They

include things such as retained profit,

working capital and sale of assets.

External and internal sources of finance can be further sub-categorised into long term and short term finance solutions but this is not particularly important for the exam.

Budgeting

A budget is a financial plan which sets out targets for company expenditure and company revenues.

Budgeting is

drawing up one of these financial plans in order to monitor the performance of

a business in sticking to the quantifiable

financial targets set out by a budget. Budgeting is an integral and

important source of financial control.

Budgets are also another way of controlling cash flow more effectively and in some ways are practical solutions to problems highlighted by cash flow forecasting.

Of course budgets have their advantages and disadvantages. One advantage of budgeting for example is that can work as a way of cutting the entire cost base of a particular organisation. A disadvantage may be however that financial allocations are too generous for a particular budget which leads to inefficient use of company cash. These problems can be overcome by flexible budgeting and zero budgeting, where all expenditure must be justified to ensure allocations are not excessive for any particular section of a budget.

Cost Centres and Profit Centres

Cost centres and profit centres are specific parts of

organisations which are created in order to exert budgetary control in a

practical manner on that organisation. A cost centre is a department for which

costs can be solely calculated, whereas a profit centre is allocated

responsibility for revenue and costs and hence is able to calculate overall

profit.

|

Advantages of Cost/Profit centres |

Disadvantages of Cost/ profit centres. |

|

|

Variance Analysis

The final aspect of the course which you will need to be familiar with for the exam is what is known as variance analysis. Variance analysis is something which staff in a profit or cost centre would need to use when analysing the budgets for their company. Variance is basically the difference between forecasted financial targets and actual outcomes. Variance can be good (FAV) or bad (ADV) short for favourable and adverse respectively. If asked to annotate a profit/loss account you must remember these two terms as they are the only terms you are allowed to use to represent whether a company has made a profit or a loss. Remembering FAV and ADV will allow you to pick up some easy marks if this sort of question were to come up.

That’s it for Business Studies Module 1 well done and good

luck in your exam, hope I’ve helped to clarify the major aspects of this topic

for you all.