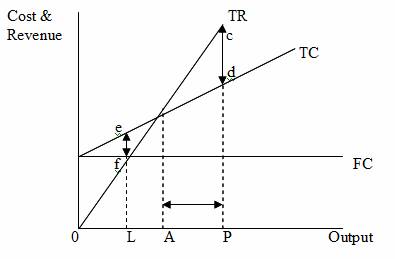

Break Even Analysis: Break-Even Charts

This at the moment probably means nothing to you but

this description should help to clear things up:

- The

Break- even output is at A (See

calculating Break even output)

- The

distance AP represents the margin of safety if the firm is producing

at P

- The

distance cd represents the profit made if output is at P

- The

distance ef represents the loss made if production is at L

- FC

is Fixed Costs

- TC

is Total Costs

- TR is Total Revenue

Calculating Break-Even Output

The amount of money left over once variable costs have been covered.

For Break Even Output we need to know a slightly more specific form of contribution which is called Contribution per unit. This is worked out as follows:

Contribution per unit = Price Average Cost

(Revenue

per unit) (Cost per unit)

Note: Average cost is sometimes called variable cost per unit as well.

Now your ready for the Break even output formula- brace yourselves its a bad boy.

Heres a quick example. Price = £17 Average Cost = £9 Fixed Cost =£1456

This means that for this particular product to break even 182 will have to be sold.